César Ramos | Global IFRS 9 & Hedging Expert

Stop P&L Volatility. Start IFRS 9 Compliance.

The IFRS 9 Hedging Quick Start Toolkit is the fastest way for SMEs to implement audit-proof Hedge Accounting—without hiring a Treasurer.

Figure 1: Streamline Audit Process

Stop the friction between your team and the auditors. Our Framework streamlines the process.

View the Quick Start Toolkit & Pricing

Need custom implementation? Book a Remote Strategy Session.

Your Business Solves Three Core Problems Instantly:

1. P&L Stabilization

Our Spot-to-Spot methodology prevents derivatives’ Mark-to-Market volatility from destroying your reported profit and loss (P&L) results.

2. Audit-Proof Compliance

Go from zero documentation to full IFRS 9 compliance with our pre-built Designation Memos and Hedge Effectiveness Checklists, validated by an experienced Auditor.

3. FX Risk Management (Quick Start)

Implement a robust, professional hedging function in weeks, not months. The Toolkit acts as your outsourced Treasury procedure manual and calculation engine.

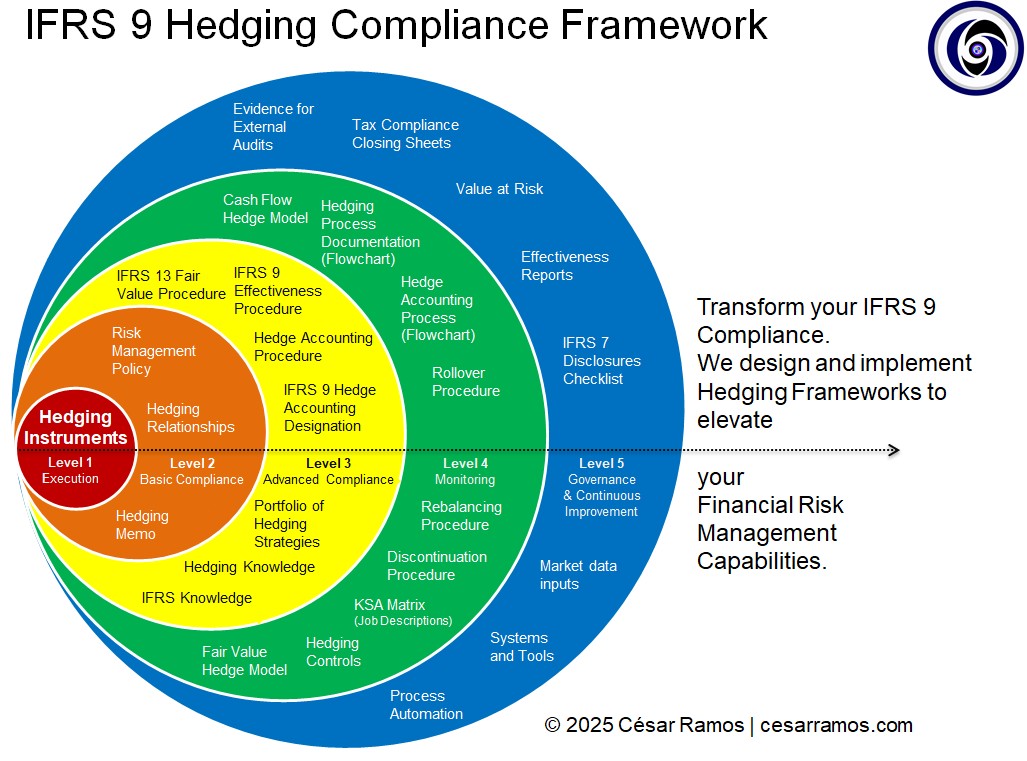

Our Proprietary IFRS 9 Compliance & Maturity Framework

The Toolkit covers Levels 1 to 3 and partially Level 4, providing all the necessary models and documentation for Full Procedural Compliance.

The Toolkit delivers Levels 1, 2, and 3. Full maturity (Level 5) is achieved through our Premium Services.

Meet Your Expert: César Ramos

I empower growing businesses to quickly implement robust risk management, mitigate FX risk, and stabilize P&L results. I deliver audit-proof compliance using the IFRS 9 Spot-to-Spot method.